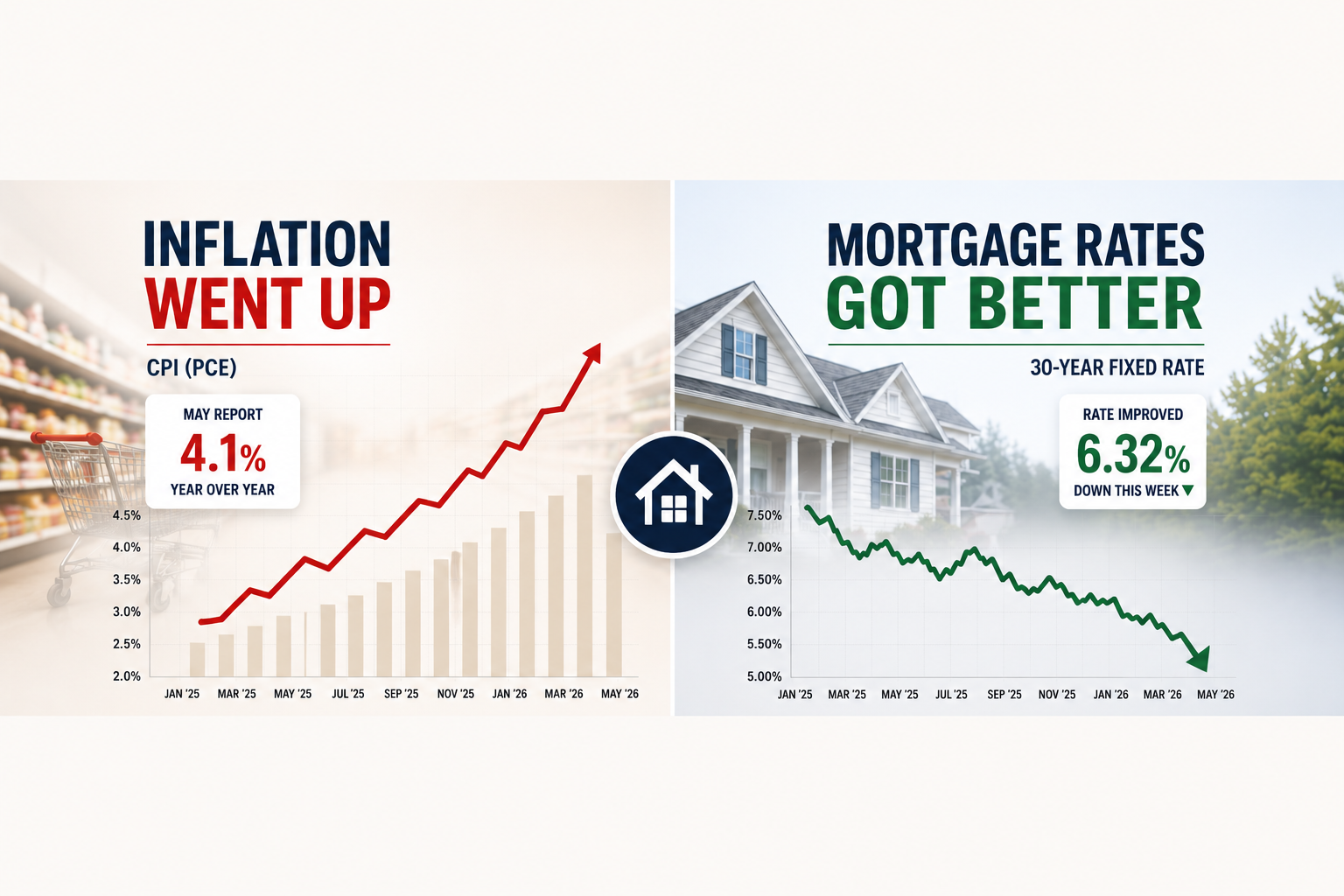

Hot inflation usually means higher rates. That's the rule, right? Except this week, the May PCE inflation report showed inflation jumping to 4.1% year over year, and mortgage rates actually got better. If you're a firefighter, first responder, or anyone shopping for a home loan right now, that probably feels like a contradiction. It isn't. Here's what actually happened, and why it matters for your rate.

Why a Hot Inflation Number Didn't Push Rates Higher

The short version: oil drove the spike, and oil has already fallen sharply. Markets price the future, not the past.

The May PCE report showed headline inflation up 0.4% for the month, climbing from 3.8% to 4.1% year over year. That sounds bad. But when you strip out food and energy, core inflation came in much milder, around 0.22% for the month. That's the number bond traders cared about.

Here's the key detail. Oil was the main culprit behind that 4.1% headline. And by the time the report was published, oil had already fallen more than $30 from where it was when the data was collected. Traders looked at the "hot" number, checked where oil is now, and priced the future, not the rearview mirror.

Mortgage bonds moved higher. Rates improved.

That's how this works.

Mortgage Rates Don't Follow Inflation Headlines, They Follow Bond Markets

A lot of buyers assume the Fed controls mortgage rates. Or that a bad CPI or PCE print automatically kicks rates up the next morning. Neither is quite right.

Mortgage rates are tied most closely to mortgage-backed securities (MBS), which trade in the bond market. When bond prices rise, yields fall, and mortgage rates tend to follow them down. When bond prices drop, yields rise, and rates go up.

The Fed sets the federal funds rate, which is an overnight lending rate between banks. That matters to your home equity line of credit, your car loan, your credit card. But for a 30-year fixed mortgage, it's the bond market that calls the shot.

The Fed matters because it influences investor expectations about inflation and growth, and those expectations move the bond market. But the Fed isn't the dial. The bond market is.

What Bond Traders Actually Look At

When a new inflation report drops, bond traders aren't just reading the headline number. They're asking:

- What drove it? A spike in volatile energy prices reads differently than broad price increases across the economy.

- Is this backward-looking? If the factor that caused the spike (like oil) has already reversed, that historical data carries less weight.

- Where is this heading? Core inflation, which strips out food and energy, is a better signal for underlying price trends. At 0.22% for the month, it told a calmer story.

In this case, the headline was hot, the cause was already reversing, and core inflation was moderate. Bonds rallied. Rates improved.

What This Means If You're Buying or Refinancing Right Now

This week's move is a good example of something I tell buyers all the time: don't make decisions based on the headline. The number on the news and the number your lender quotes you are driven by different things.

Here's what's useful to take from this week:

- Rates can improve even when inflation looks bad. The mechanism matters more than the headline.

- Oil-driven inflation spikes tend to be transitory. Markets know this and price it accordingly, which is why you didn't see a rate spike despite a headline that looked scary.

- Timing based on headlines is hard to get right. Rates moved better this week. That doesn't mean they'll hold. What it means is that the picture is more nuanced than "inflation up, rates up."

The Practical Question for First Responders

If you're a firefighter or first responder shopping for a loan right now, the rate environment is one piece of the puzzle. But there's another piece that costs people more money than a quarter-point move in rates: getting the income calculation wrong.

Public-safety paychecks carry a lot of moving parts. Base pay, overtime, FLSA, strike team, out-of-county deployment, paramedic differential, holiday pay. Most lenders count the easy stuff and stop. When your overtime, differentials, and specialty pay get left out of the calculation, your pre-approval number comes in low, and you lose buying power before you've even made an offer.

That's where the real money is. Getting your actual qualifying income counted right can move your pre-approval by more than most rate fluctuations ever will.

I used to work that schedule, so I know how that pay actually stacks. Getting to your real number is part of what I do.

Get Your Actual Number

Rates moved better this week. That might create a small window, or it might not last. What I do know is that if your income isn't being counted right, no rate improvement makes up for the buying power you're leaving on the table.

No credit pull, no application to start. Send me a recent stub and two years of W-2s, and I'll get you a real number this week. If the timing's not right yet, no problem; reach out when it is.

This article is provided for general informational and educational purposes only and does not constitute financial, legal, or tax advice. It is not a commitment to lend, and loan approval, terms, rates, and the treatment of specific income types depend on individual circumstances, lender guidelines, and underwriting review. Hess Mortgages and Andy Hess do not guarantee loan approval or specific outcomes. For tax-related questions, please consult a qualified CPA or tax advisor. All loans are subject to credit approval and property appraisal. Andy Hess, NMLS #1791379. Hess Mortgages is an independent mortgage advisory serving California.